Venture capital powers some of the world's most innovative companies, but the mechanics of how it actually works remain mysterious to many entrepreneurs. If you're building a startup and considering VC funding, understanding the entire venture capital ecosystem—from how VCs raise money to how they make investment decisions—is crucial for navigating this complex landscape successfully.

What Is Venture Capital?

Venture capital is a form of private equity financing that investors provide to startups and early-stage companies with high growth potential. Unlike traditional bank loans, venture capital doesn't require repayment on a fixed schedule. Instead, VCs take equity ownership in your company, betting that your business will grow significantly and eventually provide returns through an exit—either an acquisition or initial public offering (IPO).

The fundamental premise is simple: VCs invest in high-risk ventures that banks won't touch, accepting that most investments will fail in exchange for the possibility that a few will generate outsized returns. This risk-reward dynamic shapes everything about how venture capital works.

How Venture Capital Firms Raise Money

Before venture capitalists can invest in your startup, they need to raise money themselves. This process is often invisible to founders but fundamentally impacts how VCs operate.

Venture capital firms raise funds from limited partners (LPs)—institutions and wealthy individuals who commit capital to VC funds. These LPs include university endowments, pension funds, insurance companies, foundations, and family offices. A typical VC fund might raise anywhere from $50 million to several billion dollars, depending on the firm's track record and strategy.

The fundraising process for VCs can take six months to a year. They pitch their investment thesis, demonstrate their track record, and explain their strategy to potential LPs. Once they've secured commitments, they close the fund and begin deploying that capital over the next 3-4 years.

Here's where it gets important for founders: VCs don't receive all the committed capital upfront. Instead, LPs make "capital calls" when the VC firm identifies investment opportunities. This structure means VCs must maintain good relationships with their LPs and deliver on their promises, or they'll struggle to raise future funds.

The Venture Capital Fund Structure

Understanding fund structure explains many VC behaviors that might otherwise seem puzzling. A typical venture capital fund operates on a 10-year lifecycle, though this can be extended by a few years.

Years 1-4: The investment period, when the VC actively deploys capital into new companies. This is when they're most actively seeking deals and writing checks.

Years 5-10: The harvesting period, when the focus shifts to supporting existing portfolio companies and seeking exits. VCs typically aren't making new investments during this phase, which is why understanding a firm's fund lifecycle matters when you're fundraising.

VCs typically charge a management fee of 2% annually on committed capital, which covers their operational expenses—salaries, office space, travel, and due diligence costs. This fee alone doesn't make venture capital lucrative for the partners.

The real money comes from carried interest, typically 20% of the fund's profits after returning the original capital to LPs. This structure aligns incentives: VCs only get wealthy if their investments generate substantial returns. If a $100 million fund returns $300 million to LPs (a 3x return), the VC firm takes 20% of that $200 million profit—$40 million split among the partners.

How Venture Capitalists Source Deals

VCs find investment opportunities through multiple channels, and understanding these can help you position your startup more effectively.

Warm introductions remain the dominant source of quality deals. VCs trust referrals from other founders in their portfolio, fellow investors, lawyers, and executives they respect. This network effect explains why breaking into venture capital as an outsider can feel challenging—but also why building relationships matters so much.

Inbound applications through a firm's website do occasionally result in investments, but the conversion rate is low. With hundreds or thousands of pitches flooding in, it's difficult for any individual application to stand out without some context or connection.

Outbound sourcing has become more sophisticated. Many firms now employ talent partners or associates specifically tasked with finding promising companies before they formally raise capital. They track GitHub repositories, ProductHunt launches, accelerator cohorts, and industry conferences.

Co-investment networks mean VCs often collaborate, particularly at later stages. A firm that leads a Series A might bring in other firms for the Series B, creating deal flow for those partners.

The Investment Decision Process

Once a VC identifies a potential investment, they follow a fairly standard process, though timelines and rigor vary by firm and stage.

Initial meeting: Usually 30-60 minutes where you present your vision, traction, and why now is the right time for this solution. VCs are evaluating the team, market opportunity, and whether your approach is differentiated. Most opportunities end here—VCs pass on 99% of companies they meet.

Partner meeting: If there's interest, you'll present to the full partnership. This is typically a more intense session with harder questions. Partners want to understand risks, evaluate your responses under pressure, and assess whether you're someone they want to work with for the next decade.

Due diligence: For serious opportunities, VCs conduct extensive diligence. They'll talk to your customers, check references on team members, analyze your financials, review your cap table, and examine your technology. For later-stage deals, this might include hiring external consultants or industry experts. Early-stage diligence is lighter, focusing more on team and market.

Investment committee: At larger firms, there's often a formal IC where partners must make the case for investment. Smaller firms might operate more informally, but every firm has some mechanism for collective decision-making.

Term sheet: If approved, the VC presents a term sheet outlining the key economic and control terms. This is typically non-binding except for exclusivity and confidentiality provisions. Negotiation happens here on valuation, board seats, liquidation preferences, and protective provisions.

Legal documentation: Once you agree on terms, lawyers draft the detailed agreements—Stock Purchase Agreement, Investors' Rights Agreement, Voting Agreement, and amended Charter. This process typically takes 2-4 weeks.

Venture Capital Investment Stages

Venture capital operates across distinct stages, each with different risk profiles, check sizes, and expectations.

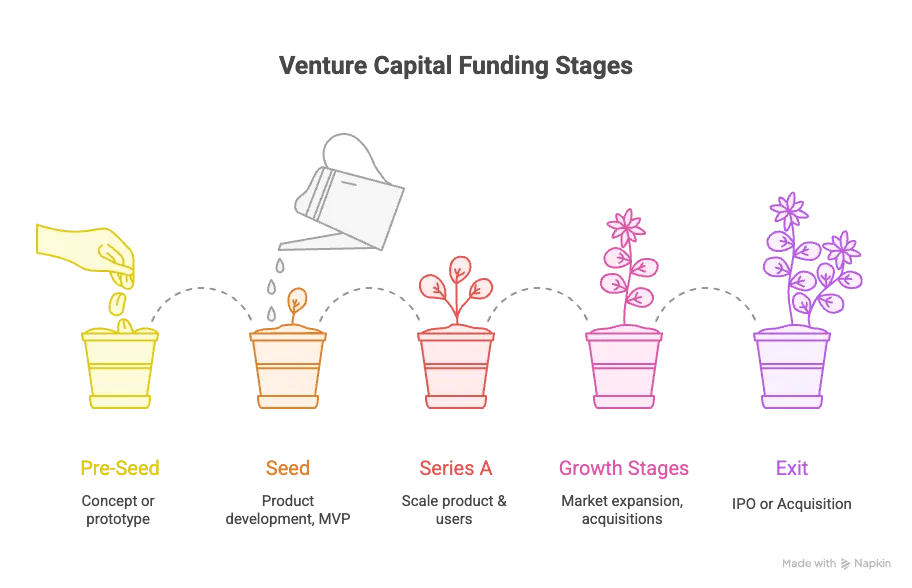

Pre-Seed and Seed Stage

The earliest institutional capital, typically $500K to $3 million. At this stage, you might have a prototype and early user feedback, but rarely significant revenue. VCs are betting primarily on the team and the size of the opportunity. They expect most seed investments to fail but hope a few will become breakout successes.

Series A

Usually $5-15 million, Series A investors want to see product-market fit. You should have clear evidence that customers want your product—typically hundreds of thousands to low millions in ARR for B2B companies, or strong user growth and engagement for consumer products. The VC is betting you can scale what's working.

Series B and Beyond

Growth-stage rounds where companies raise $20-100+ million. At this point, you've proven the business model works and need capital to expand—new markets, new products, larger sales teams. The risk profile is lower, but so are the potential returns relative to earlier stages.

How Venture Capitalists Evaluate Investments

VCs look at similar factors regardless of stage, though the weight given to each shifts as companies mature.

Team: This is paramount, especially early. VCs want founders who are smart, resilient, coachable, and have relevant domain expertise. They're assessing whether you can recruit talent, evolve as a leader, and maintain composure through inevitable crises.

Market size: VCs need massive markets to generate fund-returning outcomes. A great team in a small market can build a nice business but won't deliver the 100x returns that venture capital requires. They're looking for markets that are either already large or will become large through technology-driven change.

Product differentiation: What's your unfair advantage? Why will you win against existing competitors and well-funded new entrants? VCs want to see genuine innovation—technology moats, network effects, or unique go-to-market strategies.

Traction: Evidence that your approach is working. This looks different by stage but might include revenue growth, user engagement metrics, customer retention, or strategic partnerships.

Business model: How will you make money, and can it be profitable at scale? VCs increasingly care about unit economics, even at early stages.

Competitive landscape: Who else is solving this problem? What happens if Google or Amazon enter your market? How do you stay ahead?

The Venture Capital Return Model

Understanding how VCs think about returns explains behaviors that might otherwise seem irrational. Venture capital funds need exceptional winners to overcome their many losses and generate attractive returns for LPs.

A typical VC portfolio follows something like this distribution:

- 50% of investments fail completely (0x return)

- 30% return 1-2x (modest success but below fund expectations)

- 15% return 3-10x (good investments that help the fund)

- 5% return 10x+ (the fund-returners that make or break overall performance)

This math explains why VCs push for aggressive growth even when slower, more sustainable paths might seem wiser. They need home runs, not singles. A company that generates a solid 3x return barely moves the needle for the fund, while one 50x return can make an entire fund successful.

For a $100 million fund to achieve a 3x return (considered good performance), it needs to return $300 million. After accounting for failures and mediocre performers, the fund needs 2-3 massive winners. This is why VCs often encourage "go big or go home" strategies and why they might push you to take on more risk than feels comfortable.

How Venture Capitalists Add Value

Good VCs do more than write checks. They provide various forms of support that can meaningfully accelerate your company's growth.

Strategic guidance: VCs have seen similar situations play out dozens of times. They can help you think through pricing strategies, hiring plans, fundraising timing, and competitive positioning. They often have strong opinions (which you should evaluate critically) but can provide valuable perspective.

Network access: Introduction to potential customers, recruiting candidates, future investors, and acquisition targets. The strength of a VC's network varies dramatically and is worth evaluating during diligence.

Operational support: Some firms like Andreessen Horowitz have built extensive platform teams—recruiting, marketing, technical infrastructure—that portfolio companies can leverage.

Future fundraising: Your existing investors' participation in future rounds signals confidence to new investors. Strong VCs can help you raise subsequent rounds more easily.

Crisis management: When things go wrong—and they will—experienced VCs have navigated similar situations. They can help with difficult decisions around pivots, down rounds, or even orderly wind-downs.

Venture Capital Timeline and Liquidity

One critical aspect founders often underestimate: venture capital is patient money, but not infinitely patient. VCs typically expect some path to liquidity within 7-10 years of investment.

This timeline pressure shapes many decisions. If you're building something that will take 15 years to mature, venture capital might not be the right financing source. Similarly, if you want to build a profitable $10-20 million annual revenue business with no exit plan, bootstrapping or alternative funding makes more sense.

The exit matters because that's when VCs and founders alike realize returns. Until an acquisition or IPO, everyone owns paper that might become valuable or might become worthless. This shared uncertainty usually aligns incentives, but conflicts can emerge if founders want to stay independent while VCs push for exits.

The Venture Capital Economics for Founders

Understanding how much equity to give up at each stage helps you maintain sufficient ownership to stay motivated while still raising enough capital to build something valuable.

A rough rule of thumb: expect to give up 15-25% per round. Over multiple rounds, founders often end up with 10-20% ownership by the time of exit. This might sound low, but 15% of a $500 million company is better than 100% of a $5 million company.

Dilution happens not just through funding rounds but also through employee stock options. You'll need to reserve 10-20% of your cap table for current and future employees. Factor this into your planning.

Finding the Right Venture Capital Partner

With thousands of VC firms globally, finding investors who align with your stage, sector, and geography requires research. Platforms like VCDir.com aggregate information on 1,500+ venture capital firms, making it dramatically easier to identify appropriate investors, understand their investment criteria, and research their portfolio companies.

Rather than blindly reaching out to every firm, use resources to filter by investment stage, check size, industry focus, and geographic preference. This targeted approach increases your chances of finding investors who are genuinely interested in what you're building.

The right VC partner can transform your company's trajectory. The wrong one can create years of frustration. Do your homework, talk to other founders in their portfolio, and ensure alignment on vision, values, and timeline before accepting anyone's money.

Alternatives to Traditional Venture Capital

Venture capital isn't right for every company. Several alternatives have emerged:

Angel investors provide smaller amounts of capital, typically $25K-$500K, often at earlier stages than VCs. They're usually successful entrepreneurs or executives investing their own money.

Revenue-based financing allows you to raise capital in exchange for a percentage of future revenues until you've repaid a multiple of the original investment. This avoids dilution but requires positive cash flow.

Venture debt provides loans to venture-backed companies, usually alongside an equity round. It's less dilutive than pure equity but requires repayment.

Crowdfunding through platforms like Republic or Wefunder lets you raise from many small investors, though regulatory requirements and investor management can be complex.

Bootstrapping means growing without external capital using customer revenues. It's slower but gives you complete control and often forces healthy discipline around unit economics.

How Venture Capital Is Evolving

The venture capital industry continues to change in ways that affect how it works:

Larger fund sizes mean VCs need to write bigger checks and pursue larger outcomes. This has created opportunities for new seed-focused firms to fill the gap at the earliest stages.

Specialization is increasing. More firms focus on specific sectors (fintech, healthcare, climate) or stages rather than being generalists. This benefits founders who can find VCs with deep domain expertise.

Global expansion means venture capital is no longer concentrated solely in Silicon Valley. Significant ecosystems have developed in New York, London, Berlin, Singapore, Bangalore, and dozens of other cities.

New structures like rolling funds and syndicates have democratized access to venture investing, though it remains unclear whether these will generate returns comparable to traditional funds.

The Bottom Line on How Venture Capital Works

Venture capital is a powerful tool for building ambitious companies that require significant capital before generating revenue. It works through a complex ecosystem where VCs raise money from limited partners, invest in high-potential startups, provide support and guidance, and ultimately seek exits that return capital to everyone involved.

For founders, understanding this system helps you make better decisions about whether to raise VC funding, which investors to target, how much equity to give up, and what kind of relationship to build with your investors. The best venture capital relationships are true partnerships built on mutual respect, aligned incentives, and complementary strengths.

Whether venture capital is right for your company depends on your growth trajectory, capital requirements, timeline to profitability, and personal goals. For the right companies with the right founders, venture capital can provide not just money but also strategic guidance, network access, and experienced counsel that accelerates growth in ways that would be impossible otherwise.

Use resources like VCDir.com to research potential investors, understand their investment focus, and find firms that align with your vision. With information on over 1,500 venture capital firms, you can make informed decisions about which investors to approach and what to expect from the process. The more you understand about how venture capital works, the better positioned you'll be to navigate this complex landscape successfully.

Related Articles

Top Venture Capital Firms: 2025 Guide for Startups

Discover the top venture capital firms in 2025. Compare investment stages, check sizes & sectors. Research 1500+ VCs on VCDir.com to find your perfect match.

Private Equity vs Venture Capital: 2025 Complete Guide

Private equity vs venture capital explained. Compare funding stages, ROI, risk, and deal sizes. Learn which investor type fits your business in 2025.